Egypt Electricity Utility Market Analysis

Strategic Insights for the Modern Energy Landscape

A comprehensive PESTEL and SWOT analysis of Egypt's electricity sector, examining market dynamics, growth opportunities, and strategic challenges in the context of renewable energy transition.

Market Overview

Fossil Fuel Dependency

Renewable Target by 2030

Companies Under EEHC

Transmission Grid (km)

PESTEL Analysis

The PESTEL framework examines the Political, Economic, Social, Technological, Environmental, and Legal factors shaping Egypt's electricity utility market. This comprehensive analysis reveals both the structural opportunities and systemic challenges facing the sector.

Political

- •Government subsidies and reform initiatives

- •Regulatory stability and policy frameworks

- •International energy agreements

- •State-owned enterprise dominance

Economic

- •Electricity tariff adjustments

- •Infrastructure investment requirements

- •Economic growth and demand drivers

- •Foreign direct investment flows

- •Currency fluctuation impacts

Social

- •Population growth and urbanization

- •Energy access and affordability

- •Consumer behavior and demand patterns

- •Climate-driven cooling demand

Technological

- •Renewable energy integration (Solar, Wind)

- •Smart grid modernization

- •Battery energy storage systems

- •Nuclear power development

- •Green hydrogen initiatives

Environmental

- •Fossil fuel dependency (88% of mix)

- •Renewable energy potential

- •Carbon emission reduction targets

- •Climate change impacts

Legal

- •Regulatory oversight by EgyptERA

- •Investment frameworks and PPAs

- •Local content requirements

- •Environmental protection standards

PESTEL Framework Visualization

Market Data & Insights

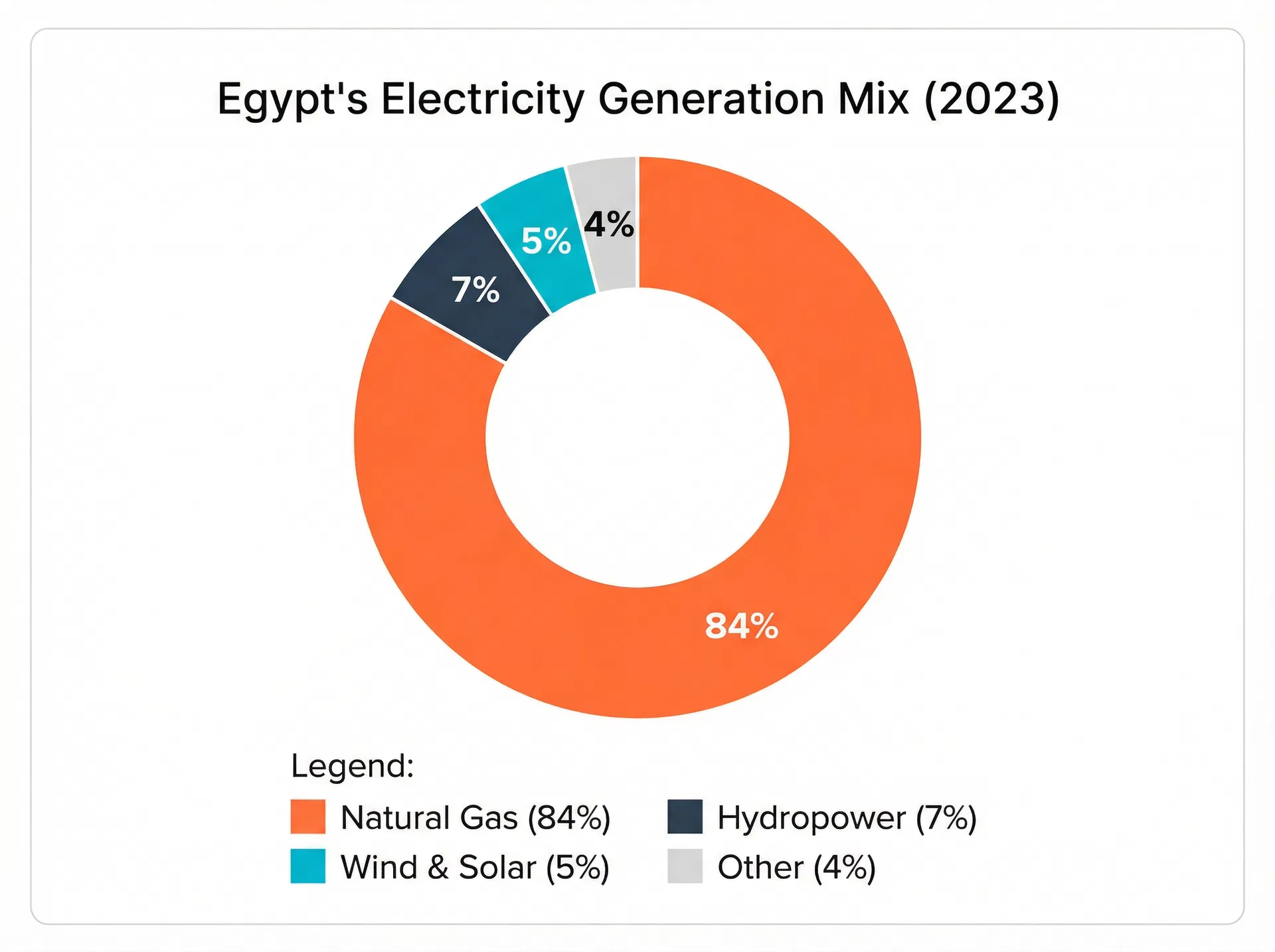

Current Generation Mix (2023)

Natural gas dominates Egypt's electricity generation, accounting for 84% of the mix. Renewable sources (wind and solar) represent only 5%, indicating significant growth potential.

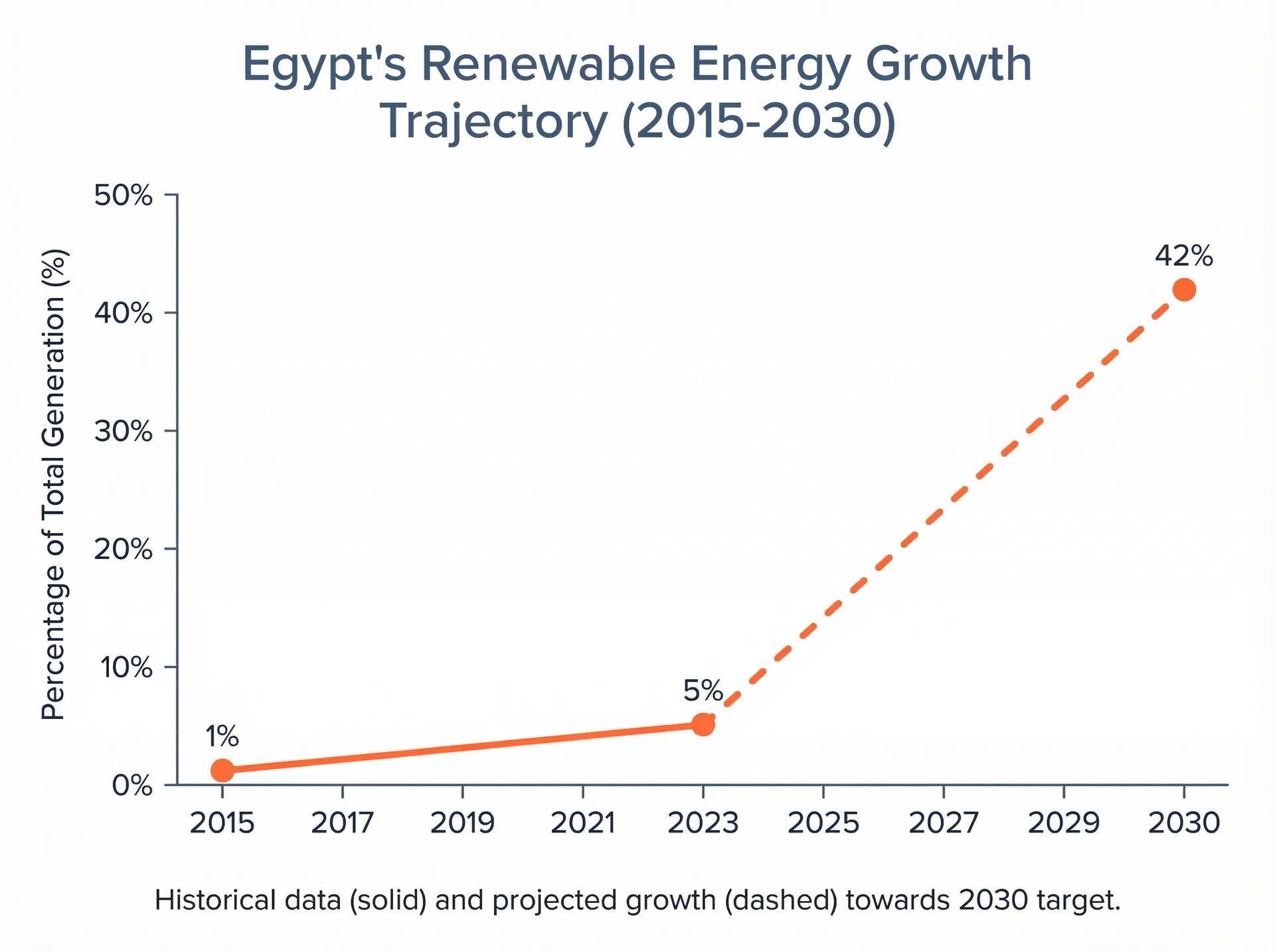

Renewable Energy Growth Trajectory

Egypt's renewable energy capacity is projected to grow from 5% in 2023 to 42% by 2030, driven by solar and wind projects and supported by government policy.

Strategic Insights & Recommendations

Renewable Energy Transition

Egypt's abundant solar and wind resources position it as a regional renewable energy leader. The 42% renewable target by 2030 requires accelerated deployment of solar and wind projects, supported by battery storage integration.

Regional Energy Hub

Cross-border interconnection projects (GREGY, Saudi Arabia, Italy) position Egypt as a strategic energy hub connecting Africa, the Middle East, and Europe. These projects unlock significant export revenue potential.

Private Sector Participation

Expanding BOO and IPP models create investment opportunities for private developers. Standardized PPAs and regulatory frameworks reduce project risk and attract foreign capital.

Grid Modernization

Smart grid technologies, including 38 million smart meters and advanced distribution control centers, improve operational efficiency, reduce losses, and enable demand-side management.

Market Structure & Key Players

Generation Companies

6 state-owned generation companies plus 1 hydropower company

- • Thermal power plants

- • Hydroelectric facilities

- • Renewable energy projects

Transmission

Egyptian Electricity Transmission Company (EETC)

- • 8,250 km of 500 KV grid

- • 35 substations (48,000 MVA)

- • 7 grid control centers

Distribution

7 regional distribution companies

- • Last-mile delivery to consumers

- • Smart meter rollout (12M of 38M)

- • Customer service and billing

Regulatory Framework

The Electric Utility and Consumer Protection Regulatory Agency (EgyptERA) oversees the sector, ensuring fair competition, pricing regulation, and consumer protection. Recent reforms have opened the market to private investment through standardized PPAs and BOO models.

Investment Opportunities

Renewable Energy Projects

Build, Own, Operate (BOO) models for solar and wind farms with standardized PPAs. Current pipeline: 1,465 MW of renewable capacity through 32 signed agreements.

- Solar parks (Benban, Kom Ombo)

- Wind farms (Red Sea region)

- Battery storage systems

Grid Modernization

Smart grid technologies, distribution control centers, and digital infrastructure. EGP 25 billion required for distribution grid upgrades.

- Smart meter deployment

- Control center construction

- IoT and digitalization

Green Hydrogen

Emerging opportunity to leverage renewable energy for hydrogen production. Target: 5-8% of global hydrogen trade by 2040, with $60 billion investment potential.

- Hydrogen production facilities

- Export infrastructure

- Technology partnerships

Regional Interconnections

Cross-border transmission projects connecting Egypt to Europe, Saudi Arabia, and neighboring countries. Massive export revenue potential.

- GREGY Interconnector (3,000 MW)

- Saudi Arabia connection (3,000 MW)

- Italy interconnector (3,000 MW)

Conclusion

Egypt's electricity utility market stands at a critical juncture, transitioning from a fossil-fuel-dependent system to a diversified, renewable-focused energy landscape. The combination of abundant natural resources, strategic geographic location, government commitment to renewable energy, and opening to private investment creates significant opportunities for stakeholders.

Success requires addressing key challenges: modernizing aging distribution infrastructure, accelerating the phase-out of subsidies, attracting sustained foreign investment, and managing the complexities of regional interconnection projects. The next five years will be pivotal in determining whether Egypt can achieve its ambitious 42% renewable target by 2030 and establish itself as a regional energy hub.